Egypt now faces mounting pressure from a widening regional energy crisis that has disrupted fuel flows across the Gulf and beyond. Recent shocks, including reduced LNG output from Qatar, suspended Israeli gas pipelines, and ongoing instability around the Strait of Hormuz, have tightened global supply at a critical moment. Although the country has not been directly targeted, its position as a net energy importer leaves it highly exposed to these external disruptions. Egypt relies heavily on imported liquefied natural gas and pipeline gas to meet domestic demand, which means any sustained interruption quickly translates into shortages, rising costs, and growing strain on its economy.

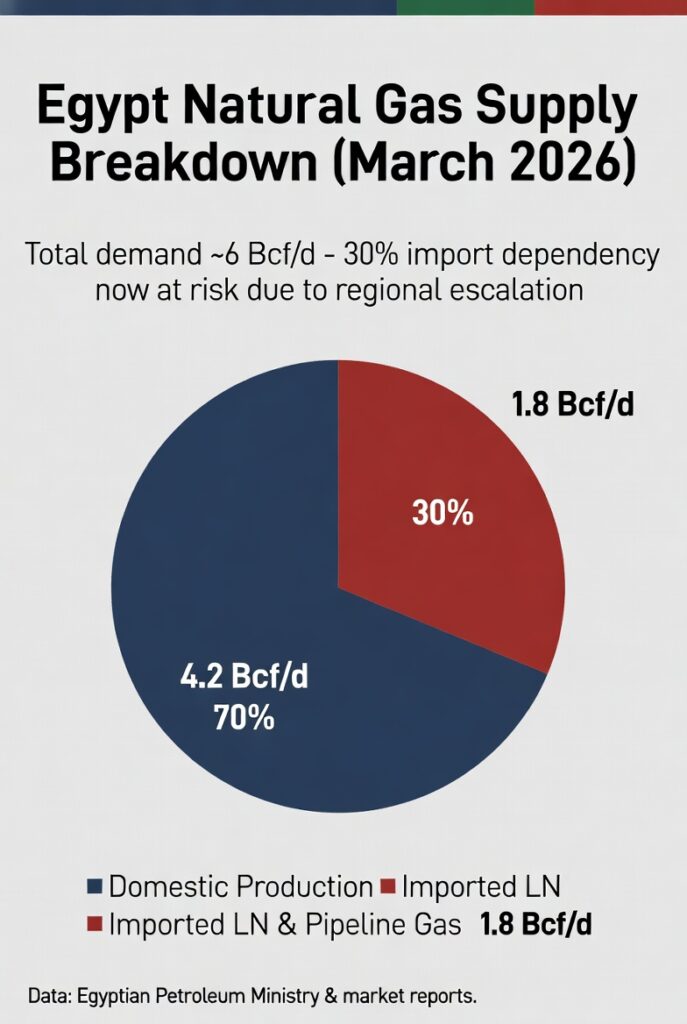

1. Egypt’s Current Energy Supply Ratio (March 25, 2026)

Egypt’s power sector is ~80% natural gas-fired. Daily snapshot:

- Domestic production: ~4.2 billion cubic feet per day (Bcf/d) — down from peak ~7 Bcf/d due to Zohr field decline and under-investment.

- Total demand: ~6 Bcf/d (power + industry + households).

- Shortfall: ~1.8 Bcf/d → 30% of supply must be imported.

- Import mix pre-crisis: ~60-70% LNG (US dominant, but Qatar was a growing term supplier), 30-40% Israeli pipeline gas (Leviathan/Karish).

- Current reality: Israeli flows suspended for security; Qatari LNG cargoes under force majeure → spot LNG market is chaotic and ultra-expensive. Egypt has already burned through inventories and is chartering emergency FSRUs, but global availability is shrinking fast.

Result: No full nationwide blackouts yet, but emergency conservation is live. PM Madbouly announced rationing effective March 28: malls/restaurants close 9 p.m., street/ad lighting cut, government offices shut 6 p.m., possible 1-2 WFH days/week. Isolated evening power cuts are already being reported in non-essential areas. Fuel import bill has tripled from ~$560 million to $1.65 billion per month.

2. Impacts Egypt Has Already Faced (as of March 25)

- Forex and budget strain: Energy import costs alone are draining reserves. EGP under fresh pressure; capital flight ~$6 billion since escalation began.

- Inflation spike: Fuel prices hiked 14-17% in recent weeks. Overall CPI already feeling the pass-through.

- Suez Canal & tourism hit: Shipping rerouting + regional fear = revenue losses already in the billions cumulatively. Easter tourism season threatened by early closures and “energy crisis” headlines.

- Power sector: Precautionary load management started. Factories still protected, but evening peaks are being shaved.

- Market reaction: Bond yields up, stock market volatile, IMF talks quietly accelerating.

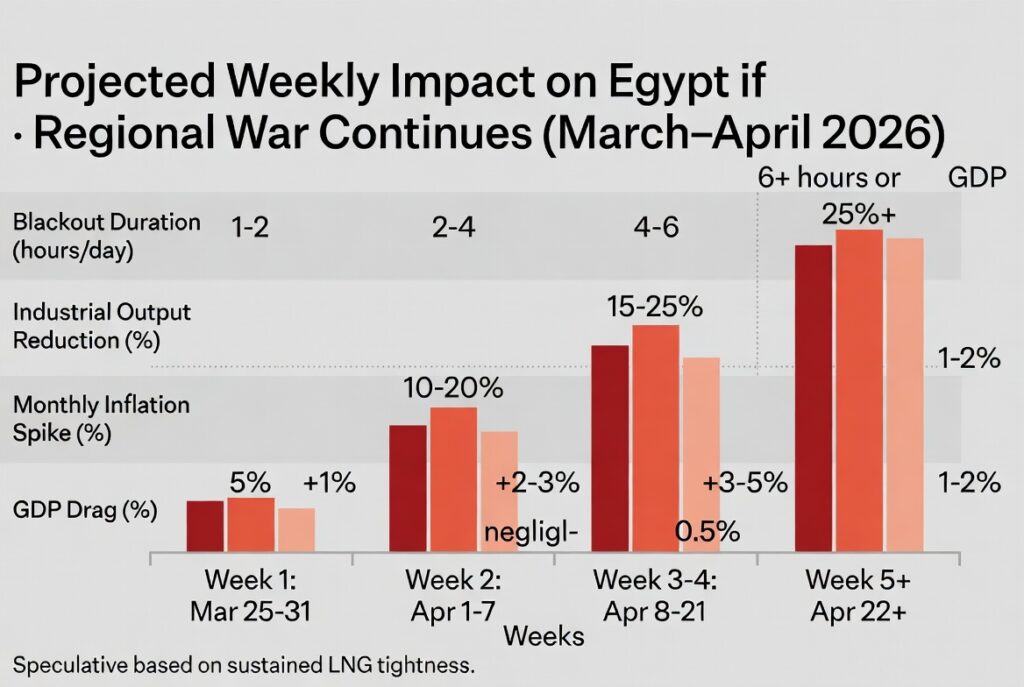

3. Weekly Projections If the War Continues (Speculative but Data-Driven)

Assuming no rapid de-escalation and sustained LNG tightness + possible further Hormuz/shipping disruption. These are incremental based on current trajectories:

| Week (from Mar 25) | Energy Supply Situation | Economic & Sector Impacts |

|---|---|---|

| Week 1 (Mar 25–31) | Rationing kicks in Mar 28. LNG deliveries ~40-50% below plan. Blackouts minimal (1-2 hrs isolated evenings). | Import bill +$300-400M extra. Inflation ticks +1%. Tourism/Suez down 10-15%. GDP drag negligible yet. |

| Week 2 (Apr 1–7) | Inventories thin; spot LNG prices +30-50%. Israeli pipeline still offline. | Rolling blackouts 2-4 hrs/day in cities. Factories start 10-20% output cuts. Fuel prices +5-8%. Subsidy bill surges. |

| Week 3-4 (Apr 8–21) | If no new US/European cargoes secured → effective 20-25% gas shortfall. | Blackouts 4-6 hrs/day. Industry output -15-25%. Farming irrigation diesel rationed. Transportation fuel queues possible. Inflation +3-5% monthly. EGP devaluation pressure. |

| Week 5+ (Apr 22 onward) | Structural crisis if repairs in Qatar take years. Possible emergency imports from Algeria/Libya at premium. | GDP contraction 1-2% per month. Unemployment spike in energy-intensive sectors. Social unrest risk in urban areas. Full “war economy” measures (further subsidies cut, WFH mandates). Possible new IMF program. |

Longer-term (2-3 months): If war drags, Egypt could face chronic 20-30% energy deficit without massive diversion of global LNG (Europe/Asia competing hard).

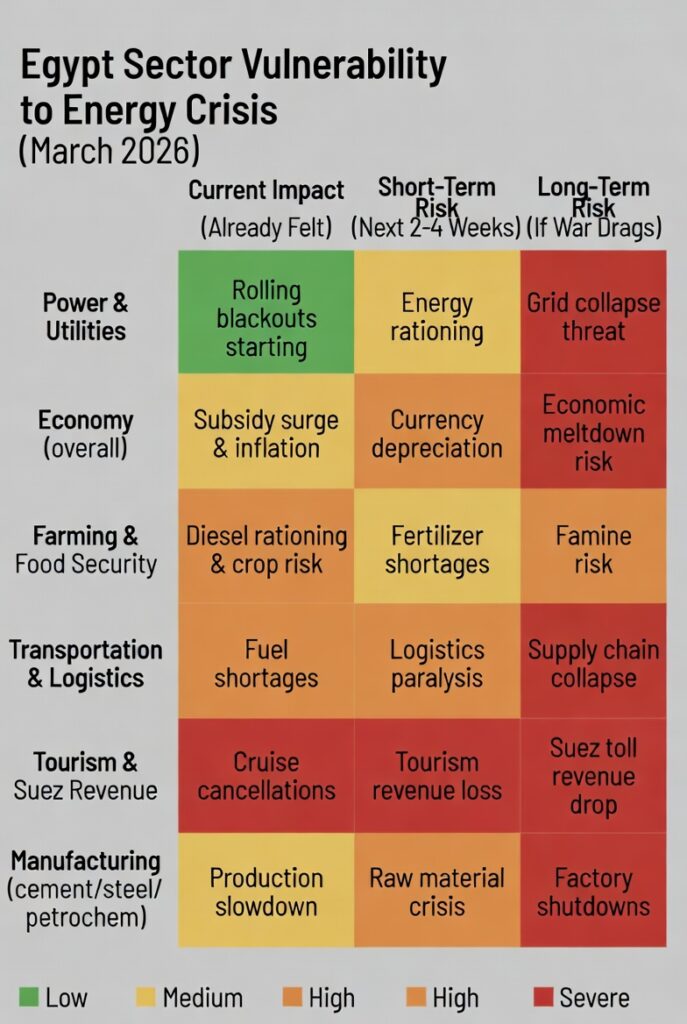

4. Sector-by-Sector Breakdown of Impacts

- Power & Utilities: Primary hit. Gas = 80% of generation. Expect rolling blackouts escalating as above. Households prioritized, but industrial tariffs likely rise 20-40%.

- Economy overall: Energy subsidies already ~5-7% of budget. Every sustained $10 oil/gas price jump adds hundreds of millions monthly. Forex reserves under threat → possible CBE rate hikes + capital controls. Growth (recently ~5.3%) could halve in Q2 if blackouts deepen.

- Farming & Food: Diesel for pumps/tractors + natural gas-derived fertilizers. Shortages = higher food prices (Egypt imports ~60% wheat). Irrigation cuts could hit summer crops (rice, cotton). Fertilizer plants already curtailing in Asia ripple here.

- Transportation: Fuel (gasoline/diesel) prices linked to global crude. Expect 10-20% pump price rises per $20 oil jump + possible rationing cards for commercial fleets. Logistics costs up → goods inflation.

- Other: Manufacturing (cement, steel, petrochemicals) output falls; remittances from Gulf workers may dip if those economies slow; tourism (key forex earner) hammered by early closures and safety fears.

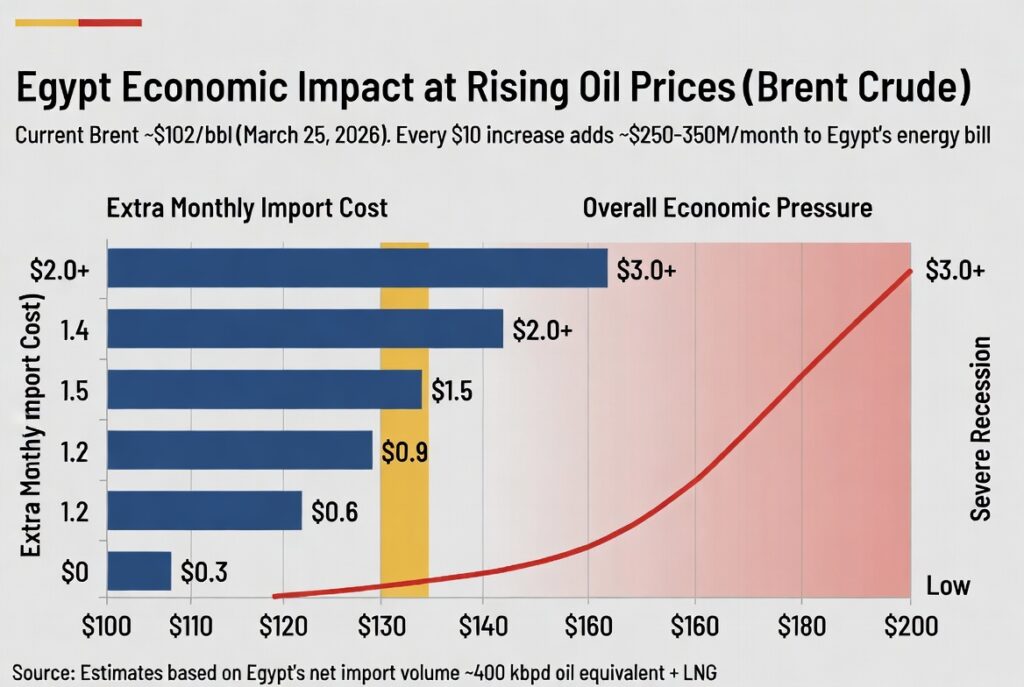

5. Oil Price Scenarios & Economic Outlook ($100 Baseline → $200 Max)

Current Brent ≈ $100/bbl (volatile; traded $98-104 today amid ceasefire hopes, but geopolitical premium remains). Egypt imports net ~250-300 kbpd oil equivalent + LNG equivalent to another ~150-200 kbpd oil. Rough rule: every $10/bbl sustained rise = +$250-350 million/month extra import bill (plus subsidy leakage).

| Oil Price Level | Monthly Extra Cost (est.) | Economic Picture for Egypt |

|---|---|---|

| $100 (current) | Baseline (already strained) | Rationing + mild inflation. Manageable with conservation & emergency LNG. Growth ~3-4% annualized. |

| $110 | +$300M | Inflation +2-3%. Blackouts lengthen. Subsidy bill +15%. EGP weakens 5-8%. IMF talks intensify. |

| $120 | +$600M | Industry slowdown 10-15%. Food/transport prices spike. Possible fuel rationing. GDP drag 1%. Social tension rises. |

| $130 | +$900M | Widespread 6+ hr blackouts. Factories at 60-70% capacity. Currency crisis risk. New emergency budget cuts. |

| $140 | +$1.2B | “War economy” declared. Tourism/Suez collapse accelerates. Unemployment +2-3%. Possible capital controls. |

| $150 | +$1.5B | Severe recession signal. Power generation -25%. Agriculture output hit hard. Debt default fears surface. |

| $160–$180 | +$2B+ | Existential for subsidies. Mass blackouts (8-12 hrs). Food shortages possible. Major social unrest risk. |

| $200 | +$3B+ | Catastrophic. Economy contracts 5-8% in months. Hyper-inflation scenario. Full reliance on Gulf/IMF bailouts. Geopolitical leverage loss. |

Bottom line: Egypt is in survival mode — not collapse yet, but the margin for error is razor-thin. The government’s early conservation moves are smart short-term damage control, but sustained war = structural energy crisis that will force painful choices (deeper subsidy reform, accelerated renewables, or heavy reliance on Gulf allies/US cargoes).

{kind=link}